Block-chain the answer for Banking KYC?

Performing KYC using blockchain technology is now a serious consideration for banks and financial institutions keen to address onboarding inefficiencies. But what are the benefits of a decentralized solution, and what are the hurdles to adoption?

- Blockchain is an ideal platform for an automated, secure, trustworthy KYC solution that improves the client experience, streamlines operations, and enhances compliance.

- The application of the technology is still nascent and untested, and there are also a number of non-technical barriers to the adoption of a KYC utility, including standardization of the data model and access to primary sources.

- A new whitepaper looks in detail at whether a blockchain-enabled KYC solution represents a new horizon or false dawn.

Anti-money laundering (AML) regulations and more stringent enforcement have led many banks and financial institutions (FIs) to err on the side of caution when conducting Know Your Customer (KYC) due diligence.

The result, in many cases, is expensive, inefficient processes that slow the pace of business and deliver a poor client experience.

Regulatory pressures have shown no signs of abating, with the 4th Anti-Money Laundering Directive now requiring data to be monitored and updated.

And the recent introduction of GDPR means FIs have to monitor their internal controls, particularly those that pertain to client data security, and to provide evidence of robust internal audits to regulators and boards.

Against this backdrop, a blockchain-enabled KYC utility model holds particular appeal, with many banks and industry partnerships exploring this option.

KYC using blockchain — benefits and barriers

Leveraging blockchain as an enablement layer in the KYC utility model could deliver trust and data security on a platform that enables efficiencies in KYC processes.

Standardizing and sharing the storage of account opening information on a blockchain creates a single tamper-proof KYC record that mutualizes the effort of conducting KYC and demonstrates compliance with AML regulations.

Several characteristics of blockchain make it a theoretically advantageous technology to leverage in the KYC space.

These include the immutability of records; enhanced privacy; a shared ledger (which improves access to accurate information across the industry); and greater transparency.

On the flip side, the application of the technology is still nascent and there are a number of dependencies required to make a blockchain-enabled KYC utility feasible, including:

- Proving the viability of the technology. To deliver a global KYC utility requires a blockchain infrastructure that can manage high levels of complexity and business logic as well as accommodate potentially thousands of nodes.

- Delivering a return on investment. The cost of developing, implementing, and migrating systems to a blockchain-enabled solution is high.

- Regulatory reform. It is essential to have support from regulators in revising guidance and regulation on this topic.

- Access to government databases. Open access to data, especially from primary sources and government databases, is critical to achieving a blockchain-enabled KYC utility and will be required in order to facilitate verification.

- Standardization of the data model. A common policy regarding identification and verification drives a common data set and realizes greater efficiencies.

Other potential barriers to KYC using blockchain include concerns around governance in a decentralized model, where there is no central party to determine standards, accept sources, or to establish the overall data model and data storage.

There are also concerns about the accessibility of the infrastructure.

For a blockchain-enabled utility to operate effectively, market-wide adoption is required across FIs, their clients, and data sources.

Engendering widespread trust in technology is another challenge.

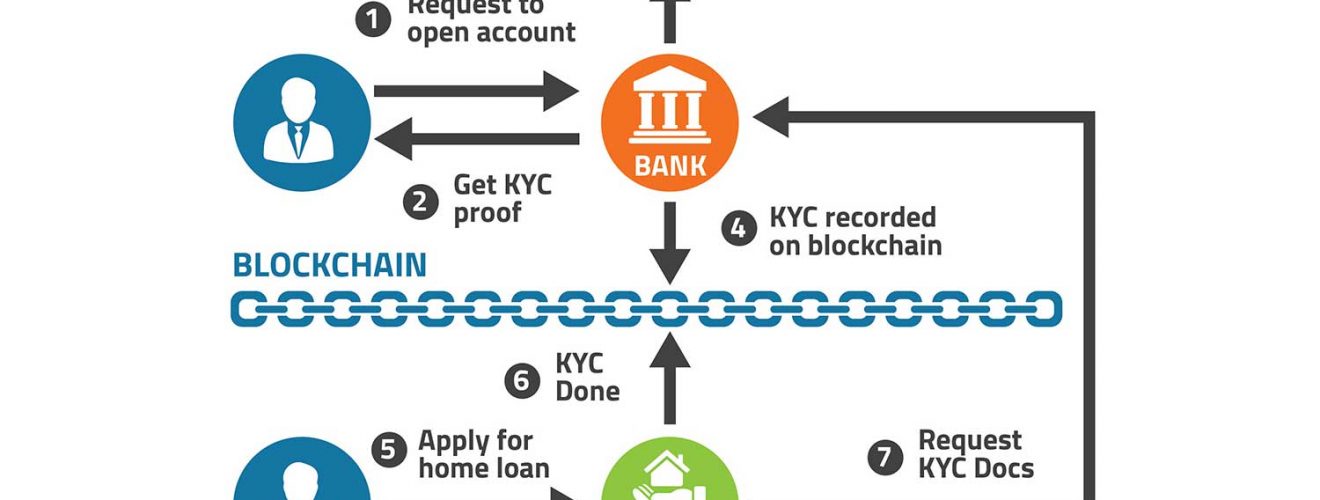

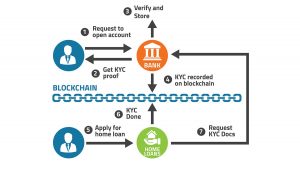

A potential model for KYC using blockchain

A potential solution for KYC using blockchain could take the following shape:

- Collection of entity data

If golden data sources, such as government agencies, create a node and provide a single authoritative source of information on a client, the requirement for the client to provide information to multiple counterparties is removed.

- Verification of entity data

Through access to primary sources and applying cryptography, identity information can be made self-verifiable, removing the need for forensic validation and allowing FIs to instantly verify identity data without having to rely on external information.

- Screening

While this process may still need to be conducted off-chain, a unique ID created for a client as part of the identification and verification process, or through existing IDs, could reduce false positives by accurately identifying the entity or individual.

- Monitoring

Creating a single record and unique ID enables FIs on the network to automatically receive updates to client entity information or changes to risk exposure.

- Reporting

This would enable an immutable audit trail of all activities relating to a KYC profile, including permissions, access and edits.

Towards a blockchain-enabled solution

Initiatives that are paving the way towards a KYC using the blockchain-enabled solution can be consolidated into two main approaches:

- The utility concept

Such a model provides an intermediary step for a blockchain-enabled KYC utility that requires many of the same considerations to be addressed — centralization; the digitization of documentation requirements; access to trusted data sources; and standardization of policy.

This still accommodates more flexibility in the model and provides a blueprint process for building trust, accelerating adoption and managing industry readiness.

- Blockchain-enabled document exchange pilots

Several technology providers, including us, are working in partnership with FIs and their end clients on piloting KYC document exchange capabilities.

These tend to leverage blockchain technology and a platform to securely store and distribute KYC-related documentation to multiple banking counterparties from a central interface.

While pilot blockchain solutions to date are solving issues surrounding data security and internal control challenges, a path towards standardization is required to address many of the other core KYC challenges.

The future for KYC using blockchain

Conceptually, blockchain provides the perfect platform to deliver an automated, secure, trustworthy KYC solution that improves the client experience, streamlines operational processes, and enhances regulatory compliance.

However, the technical challenges are not the only hurdles that the industry needs to overcome to achieve success in this space.

Solving other fundamental problems such as access to the data that would need to be distributed and stored on the blockchain, as well as harmonization of requirements across FIs and their regulators, are also precursors to success.

The utility concept is therefore still valid and a crucial component of any future blockchain solution, seeking as it does to address these issues at a global industry level.

Furthermore, blockchain technology itself is still nascent and needs to build trust in the market place to ensure adoption at scale, which in itself is critical to the success of any solution seeking to address the KYC problem.

In short, timing is everything.

Move towards KYC using blockchain too early and the inherent risks associated with the mass adoption of a new core technology could just exacerbate existing issues and slow progress.

Given the potential upside, it is critical that blockchain be part of the solution and not the problem.

Recent Comments